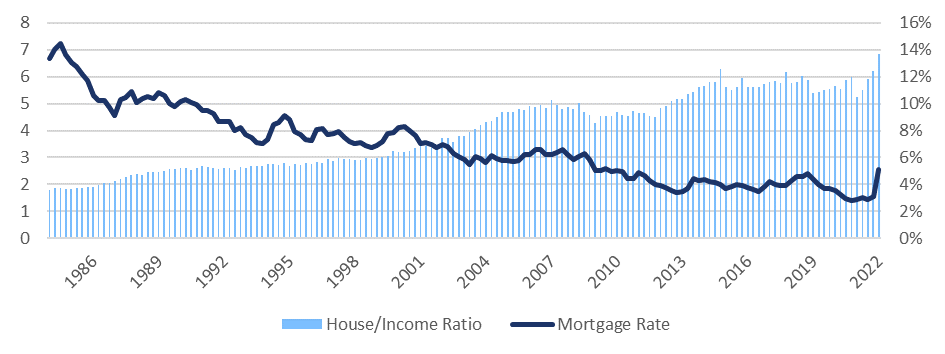

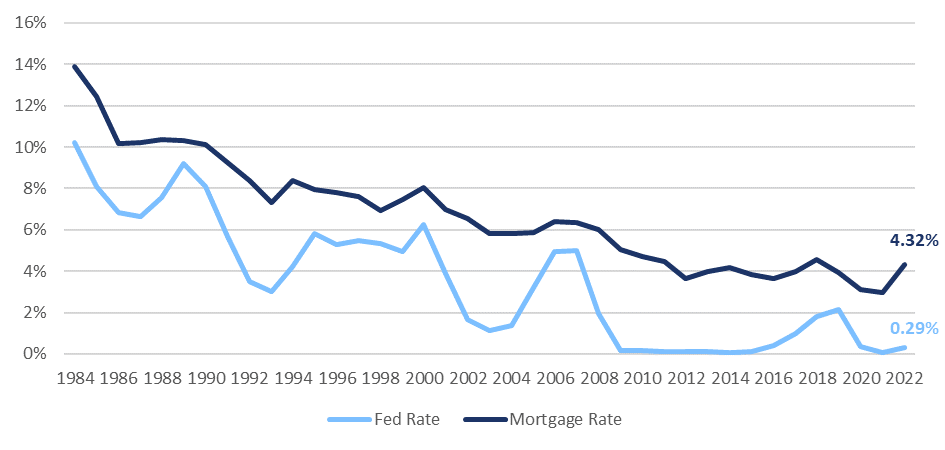

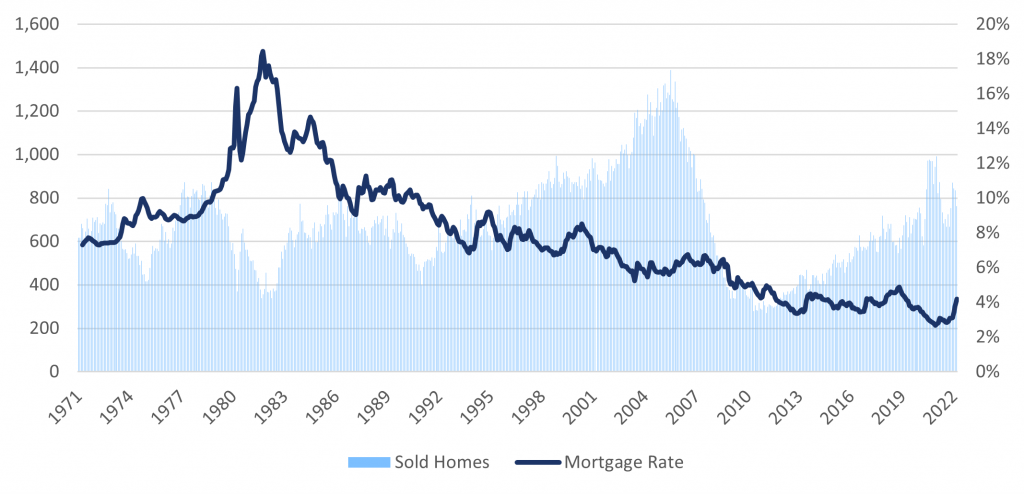

The ratio shows that real estate prices increased at a higher velocity than income. The ratio in 1984 was slightly under 2, indicating that a household needed 2 years to afford a home without any other expenses considered.

We can see that the house to income ratio increased constantly over the years, which indicates that income cannot keep up with rising house prices which means that the purchasing power of households decreased over time.

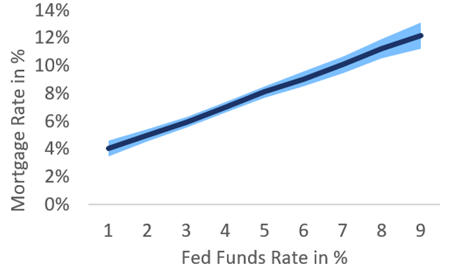

Since the financial crash starting in 2007 the ratio continued its inverse relationship with the mortgage rate to the current level, where an average household needs 6 years to afford a home. As already mentioned, until 2021 we have seen a rather negative correlation, which sounds also intuitive, as declining mortgage rates, make mortgages more affordable, thus demand for housing increases. Right now, the velocity of change significantly accelerated. As a result, private households face higher costs when financing real estate acquisitions.

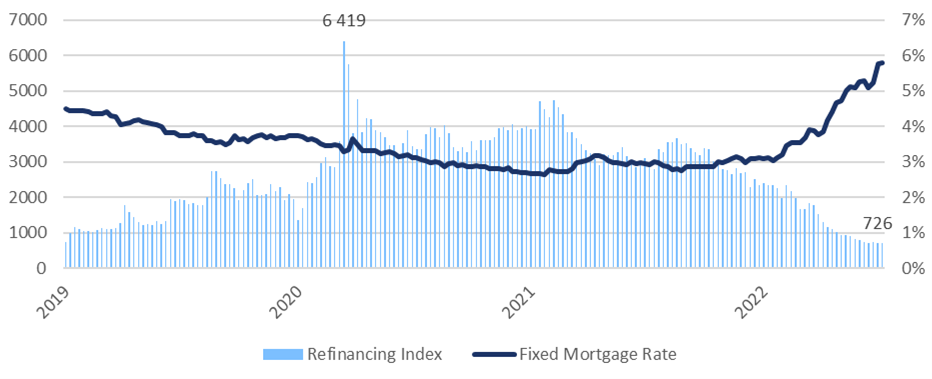

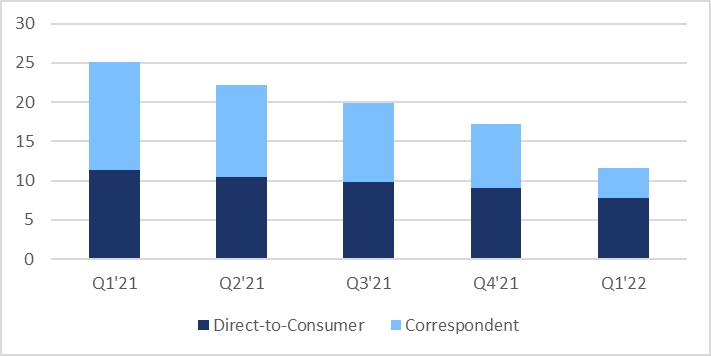

The implications of this development can be already seen in mortgage application numbers.