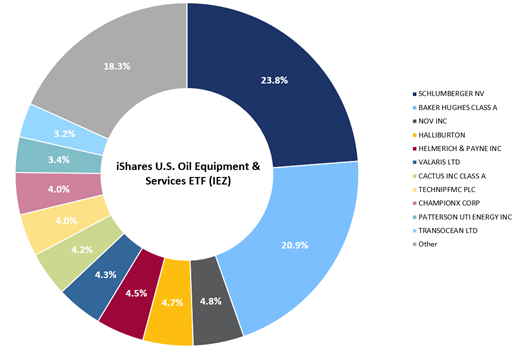

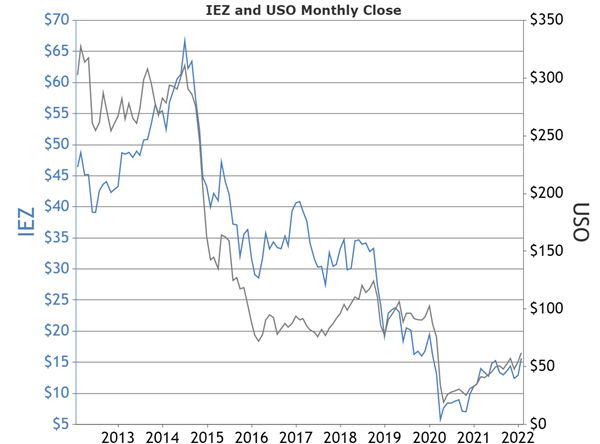

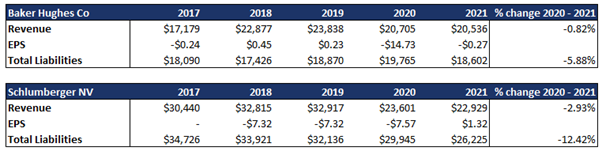

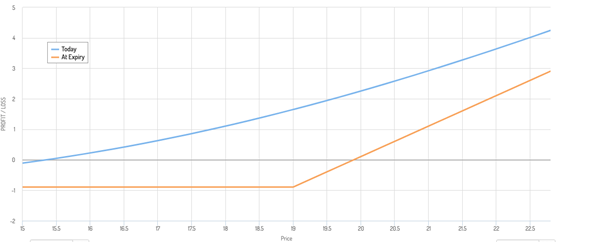

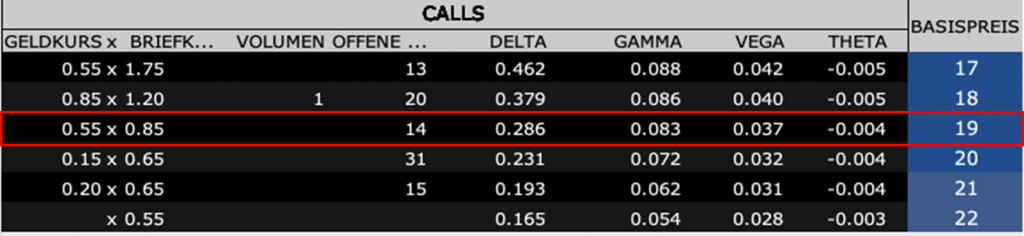

For the ETF, only buying OTM Calls seem of interest to us. Visible in the option chain, traded volume and open interest on $IEZ are extremely low, entering a suboptimal market with regards to liquidity. As the risk is to enter the trade at an unportioned high price, more complex strategies like a calendar spread or a diagonal spread currently do not present a way to trade this underlying at the moment. Consequential the profit/risk ratio is not lucrative enough, paying out low premium and coming with higher potential losses.

Nevertheless, as Schlumberger ($SLB) and Baker Hughes ($BKR) make up a significant share of the ETF, we also take a position in these holdings to support the thesis.

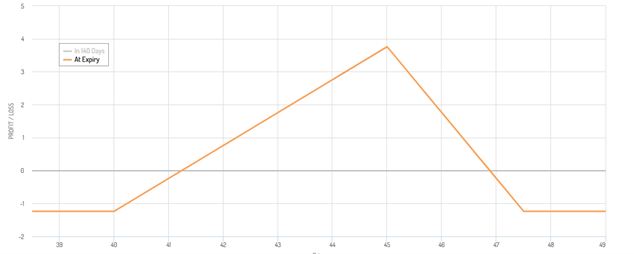

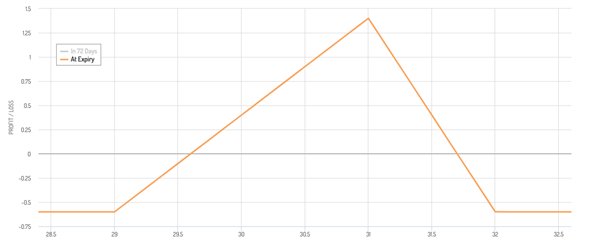

Both have more favourable volume and open Interest compared to $IEZ. Therefore, a more exotic trading strategy might fit. Christmas Tree Butterfly with calls, consisting of a long call, three higher positioned short calls and two long calls above the three sold calls. Similar to standard butterfly spreads yet giving the strategy a bullish directional exposure.

$SLB closed at $39.07. Trading the June contract (expiry: June 17th 2022), a long call at $40 with a delta of 0.53, three short calls at $45 with a delta of 0.35 and two long calls at $47.5 with a delta of 0.27. The implied volatility is at 43.6%. For this setup, a premium of $140 needs to be paid. The maximum profit is as high as $382. This results in a R:R of 2.7.