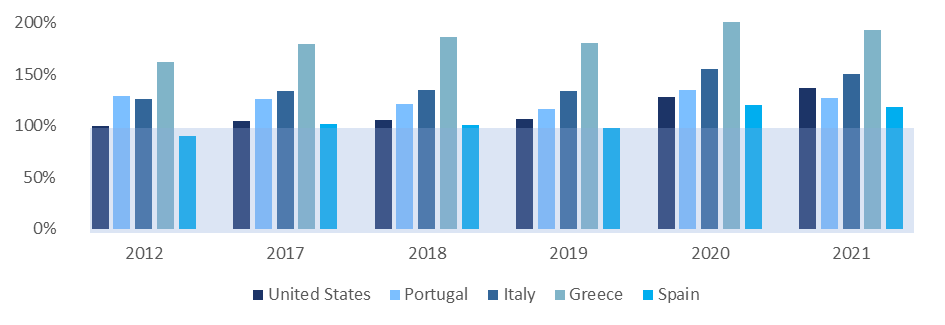

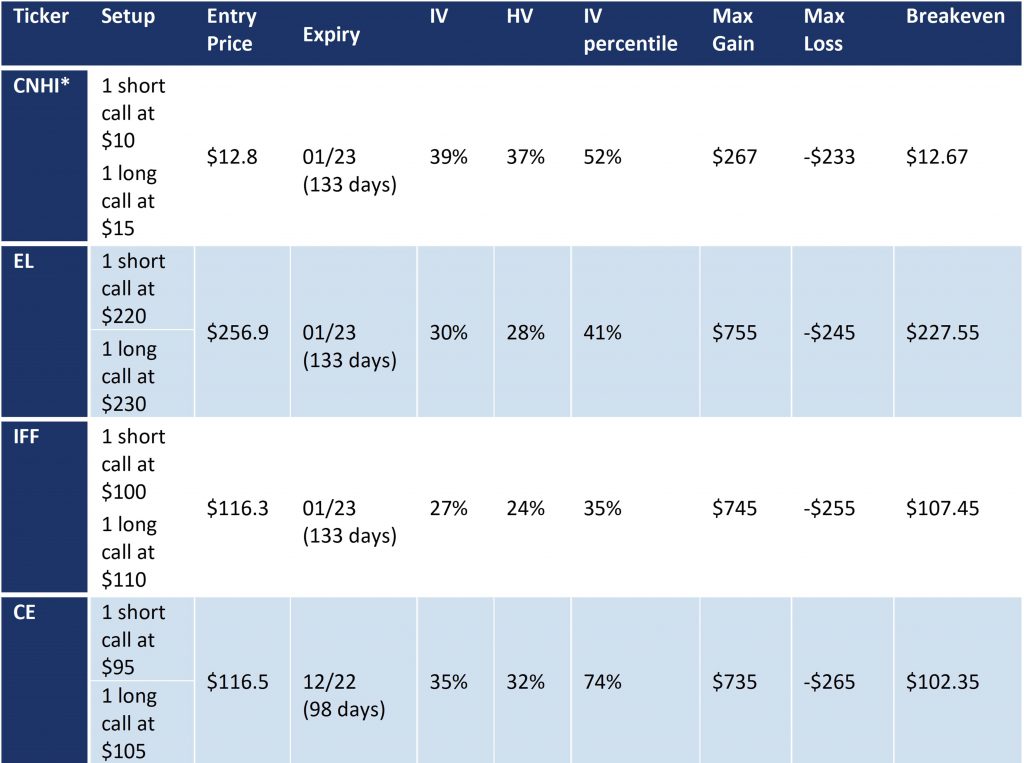

As can be seen the selected companies have made at least 38% of their revenue in Europe and with CNH Industrial we have a company which generates almost 50% of its revenue in the Euro-Zone.

It is Important to mention though, that there are also other companies with high percentage wise exposure to the Euro, though not all companies are impacted the same by the EUR/USD parity other the other mentioned factors. For this reason, we excluded companies which could be regarded as safe havens, operating in the medical space and producers of consumer goods like food, beverages and tobacco.

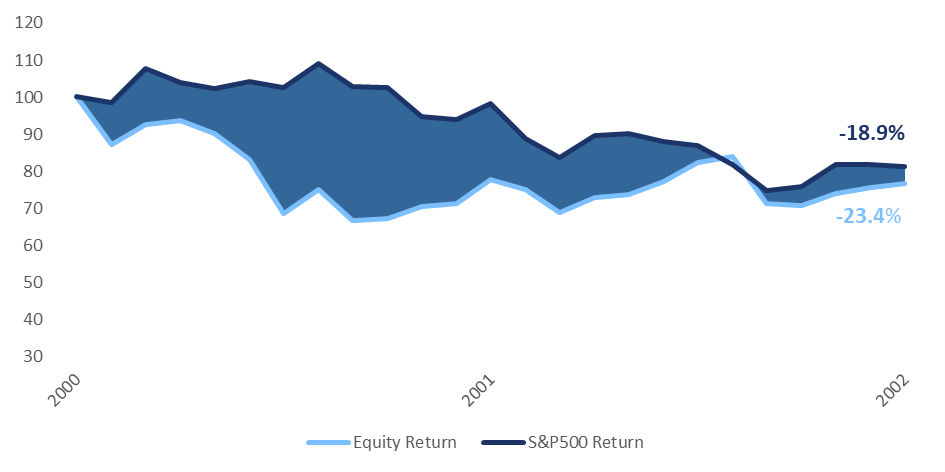

Looking at the historic performance of the respective companies compared with the S&P500 we can see that back during the time when we’ve already seen a EUR/USD parity as well as a recession, the respective companies performed considerably worse (-4.5%) than the S&P500 itself.